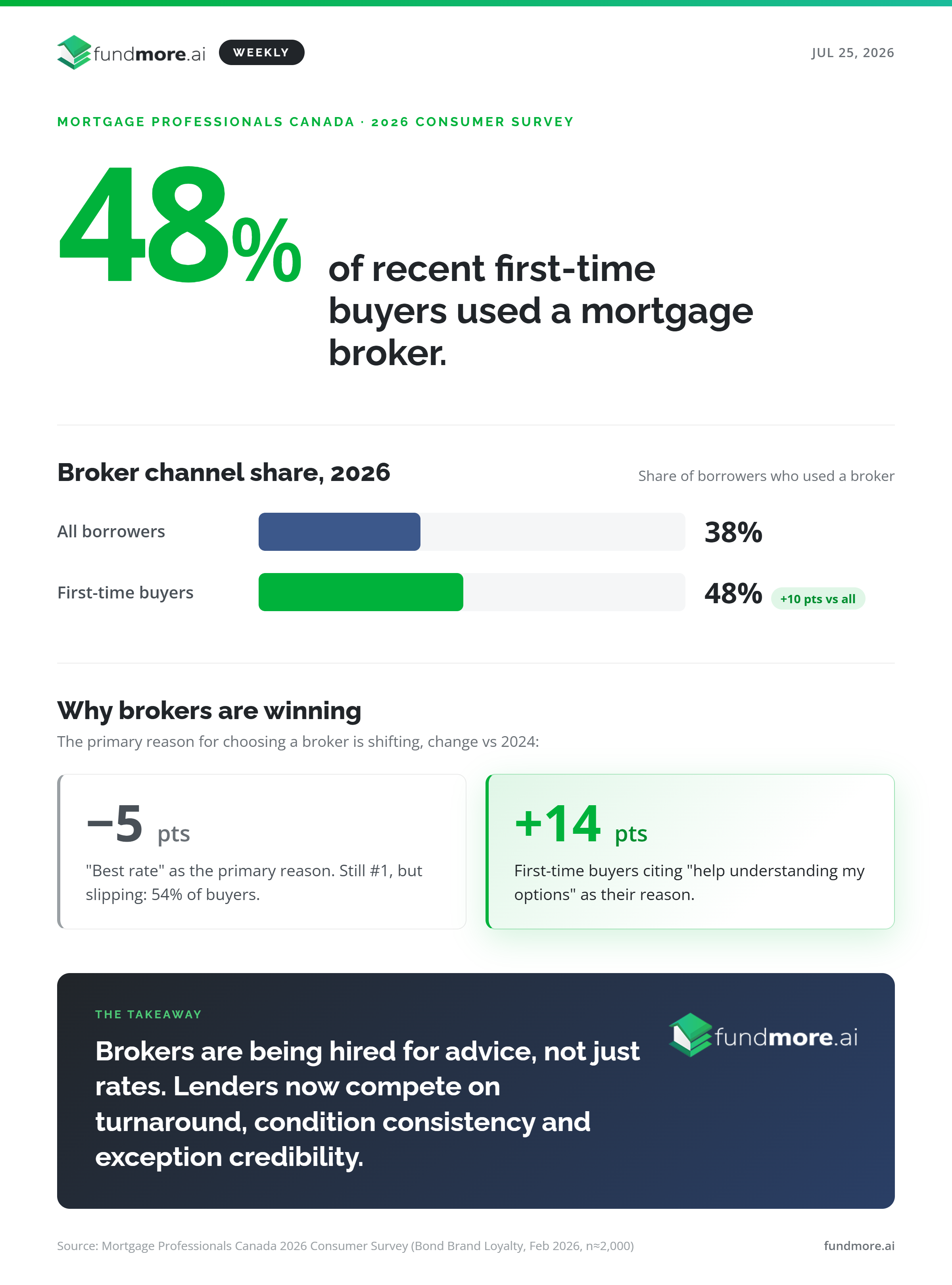

The rate era is quietly ending. The advice era is quietly beginning.

On July 24, Mortgage Professionals Canada released the 2026 Consumer Research Report, fielded by Bond Brand Loyalty across close to 2,000 Canadians in seven cities between February 5 and 25. The two headline numbers: broker channel share reached 38% overall, and 48% among recent first-time buyers. Those are not incremental moves; among first-time buyers, broker use is now within a rounding error of tied with the direct-to-lender channel that Canadian banks have owned for decades.