The polite version of a supervisory letter

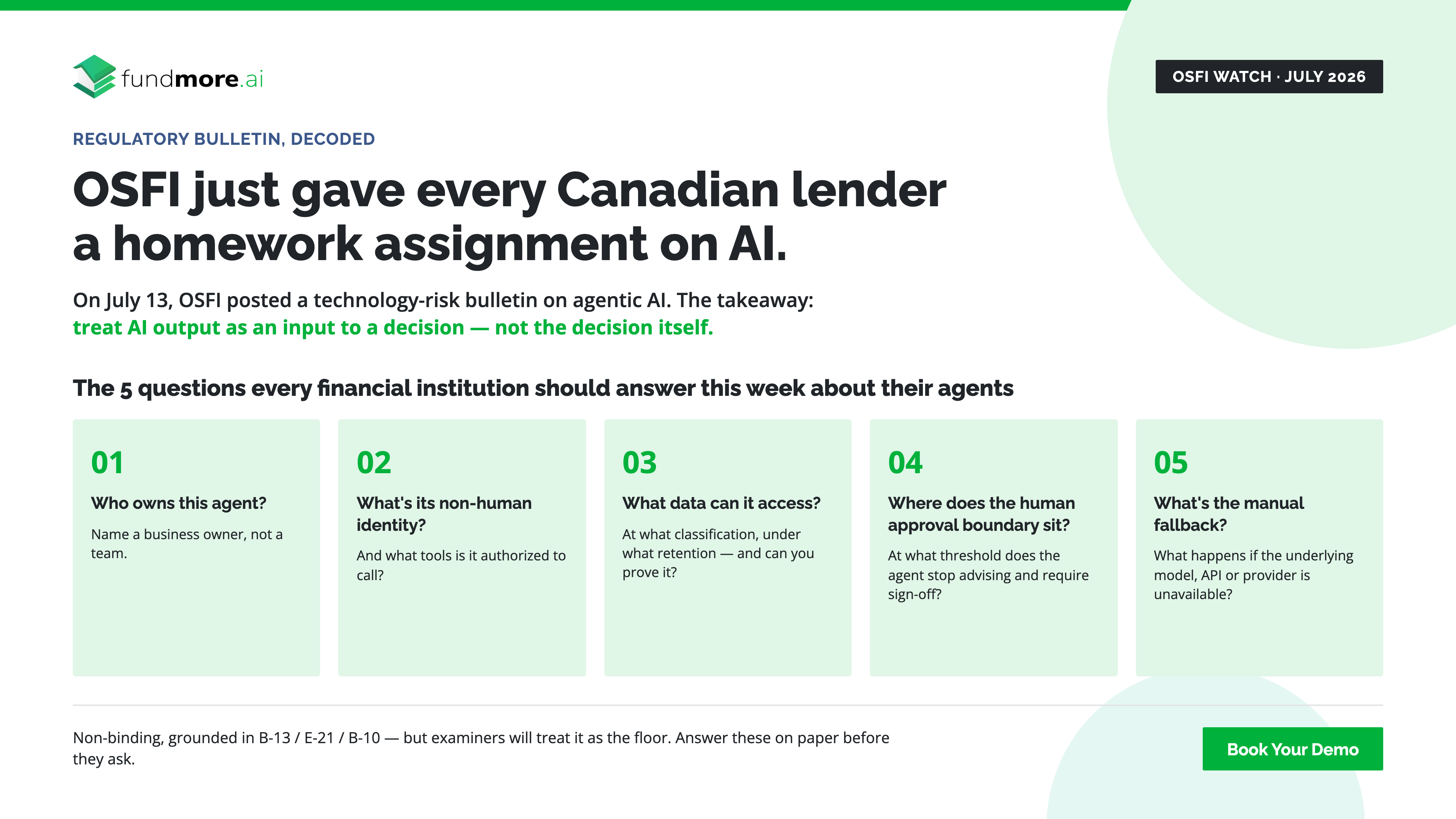

On July 13, OSFI posted a technology-risk bulletin titled Generative and Agentic Artificial Intelligence: Implications for Technology, Cyber Security, and Operational Resilience. The regulator's messaging positions it as "sound practices" grounded in the existing B-13, E-21, and B-10 guidelines, and technically, that framing is correct; no new legal duty came into force that day. Practically, the bulletin reads like the polite Canadian version of a supervisory letter: here are the questions we are going to start asking; here are the answers we would like to hear.