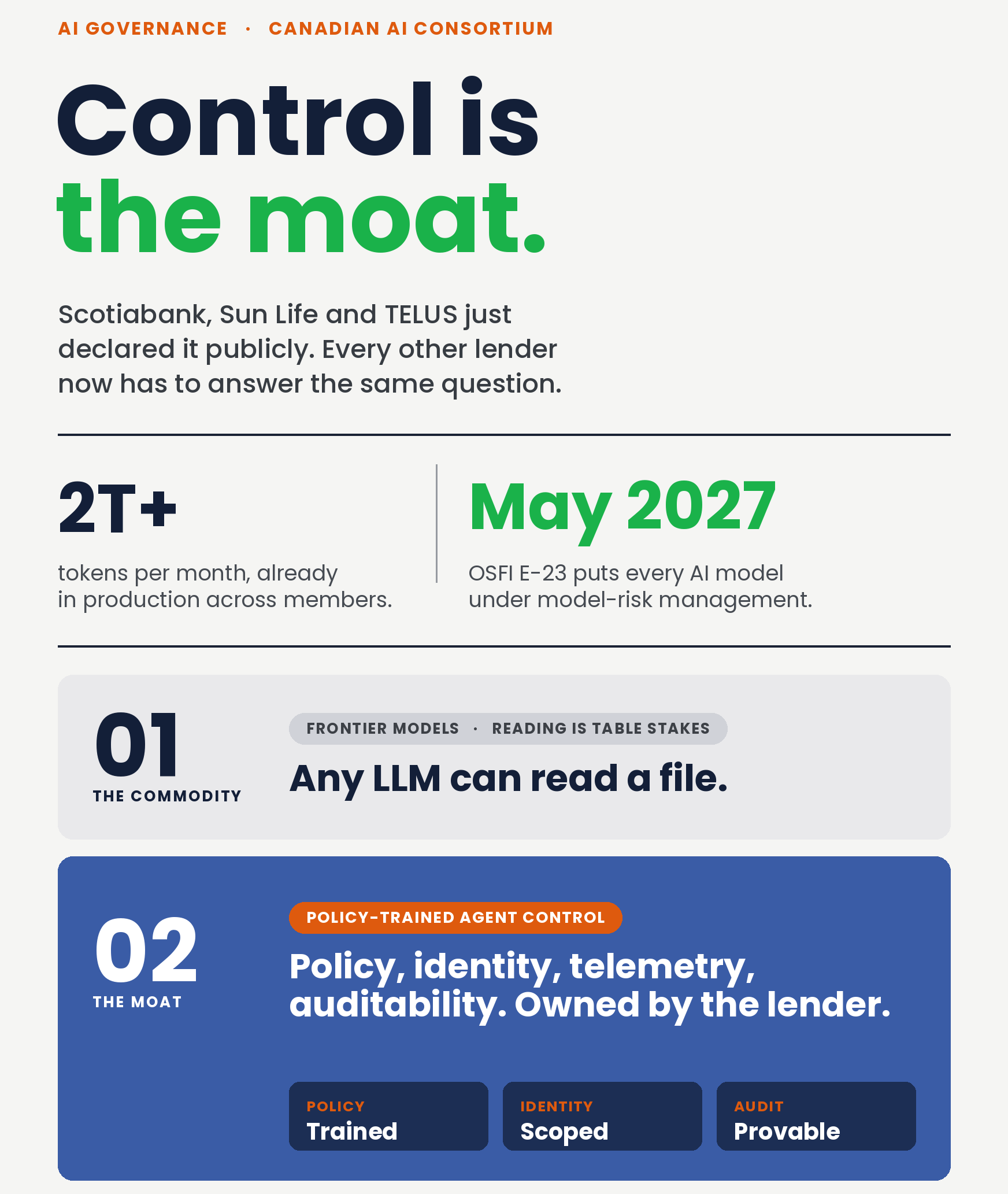

The moat moved. Most lenders have not noticed yet.

On July 7, Scotiabank, Sun Life and TELUS teamed up with Lightworks to launch the AI Consortium, a shared initiative to build and permanently own the enterprise AI control infrastructure that Canadian regulated institutions actually need. The flagship program is called the Agentic Control Plane; it is already running in production, processing more than 2 trillion tokens per month, and delivering regulatory-grade auditability across every model, agent, user and inference pipeline in scope.