The moat moved. Most lenders have not noticed yet.

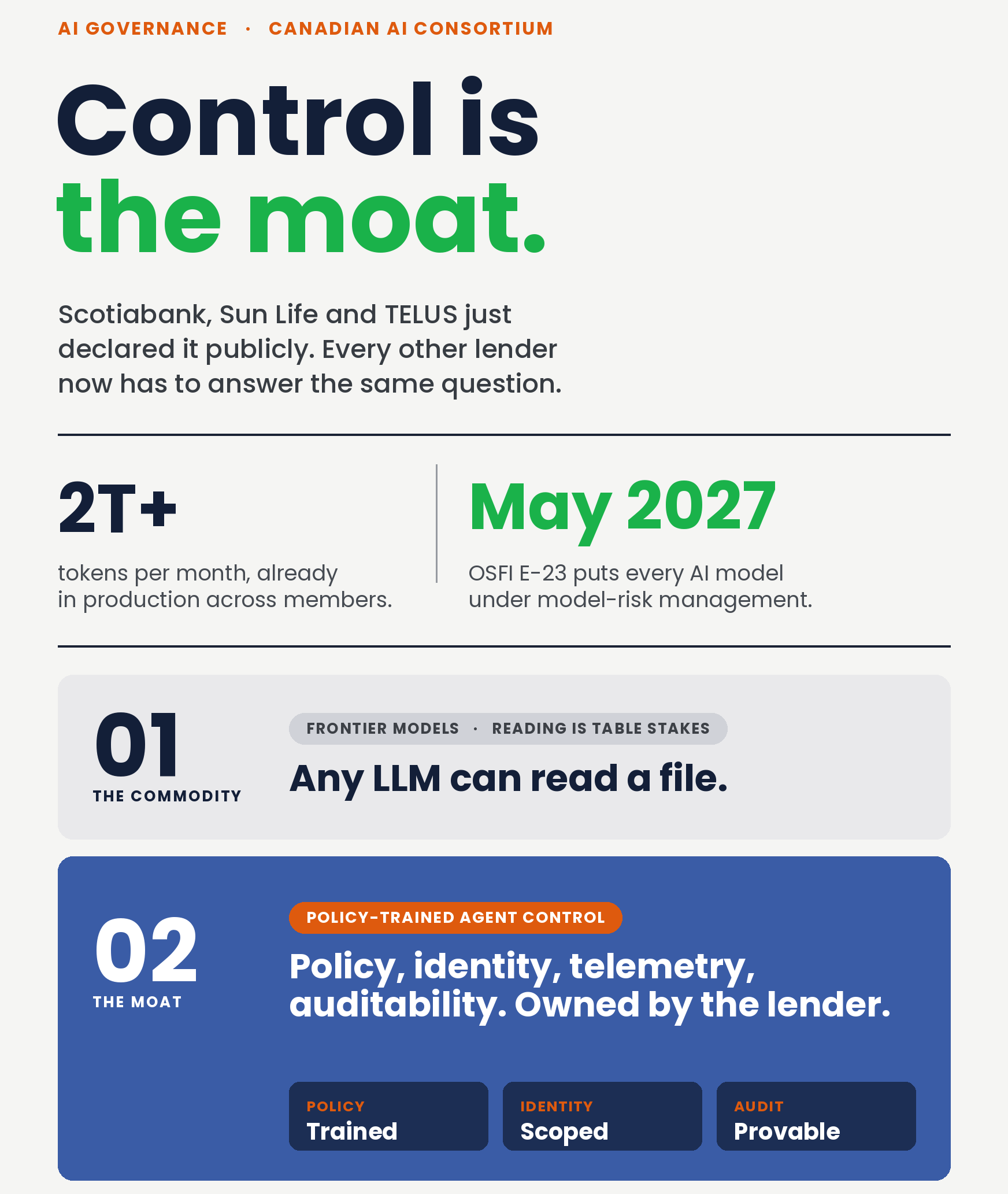

On July 7, Scotiabank, Sun Life and TELUS teamed up with Lightworks to launch the AI Consortium, a shared initiative to build and permanently own the enterprise AI control infrastructure that Canadian regulated institutions actually need. The flagship program is called the Agentic Control Plane; it is already running in production, processing more than 2 trillion tokens per month, and delivering regulatory-grade auditability across every model, agent, user and inference pipeline in scope.

The consortium's founding message is worth reading closely. TELUS CIO Hesham Fahmy called the launch "a major inflection point" and put the strategic thesis in one sentence: building AI is the easy part; governing it is the hard part. The IP belongs to members permanently, without licensing fees, dependency or kill switch. Canadian engineers, Canadian institutions, Canadian sovereignty at the centre.

Why control just became the moat

Frontier models are converging fast. Any large lender can point an LLM at a mortgage file and get a reasonable summary; that capability is now table stakes. What differs from institution to institution is what the agent is authorized to do with that reading, whose policy governs the next action, and who can reconstruct that decision two years later when a regulator or an auditor asks. That layer, the control plane, is where regulated advantage lives.

The regulators agree. OSFI Guideline E-23 now extends enterprise model-risk management to every AI and ML model at federally regulated financial institutions; compliance is due May 1, 2027, and it applies to every bank, insurer, trust and loan company OSFI supervises. Forrester formally recognized agent control plane as an enterprise product category in December 2025; by early 2026, 79% of surveyed vendors recognized it as its own tier of infrastructure.

Three questions every Canadian lender should ask this quarter

Whether or not your institution ends up joining a consortium, the Big Six just made three questions non-negotiable for your leadership team. Answer them honestly before Q3 close.

-

Identity and tool boundaries. Do you know, right now, exactly which agents are running in production, which tools they can call, and whose credit policy governs each decision? If not, you do not yet have a control plane; you have a collection of pilots.

-

Auditability and rollback. Can you reconstruct any agent decision from the last 90 days end-to-end (prompt, retrieval, tool call, policy decision, outcome) with cryptographic-grade certainty? OSFI expects yes; most lenders currently answer no.

-

Ownership and revocability. If your vendor is acquired, deprecates a model, or hits a rate limit, can you switch without breaking your production agents? If not, the vendor holds a kill switch on your underwriting.

Where FundMore fits

FundMore was designed for lenders who cannot pool engineering with a Big Five bank but still need consortium-grade discipline. Three principles govern the product.

First, policy is the moat, not the model. Every agent inside FundMore AI, FundMore IQ, FundMore QC, FundMore POS and AVA is trained on your credit policy and refined by your underwriter corrections. Frontier models are commodity inputs; the specializing signal is yours and it stays with you.

Second, digital twinning, not data pooling. Privacy-safe synthetic twins derived from platform data let you pressure-test renewal cohorts, portfolio segments and policy changes without exposing raw borrower records; the outputs are disclosed as model-derived and satisfy PIPEDA, Quebec's Law 25 and OSFI B-10 outsourcing expectations.

Third, build on existing infrastructure, not rip-and-replace. FundMore agents run on top of your existing LOS; FundMore never originates, funds or brokers, so there is no conflict of interest sitting inside your control plane. The IP that comes out of your policy tuning belongs to you, permanently, with the same "no kill switch" discipline the AI Consortium built for itself.

The next 90 days

Expect the Consortium to publish more detail on the AI Operations Center and AI Token Exchange programs, and expect the second wave of Canadian institutions to declare their control-plane strategies before year-end. Consumer-Driven Banking Regulations close consultation August 26 and will start biting inside twelve months. E-23 compliance is now a live 2027 deadline. The lenders that quietly upgrade agent governance in Q3 will meaningfully outperform peers in Q4 through renewal, retention and cost-to-serve.

See how policy-trained agents change the math on retention and workout decisioning.

Frequently Asked Questions

What is the AI Consortium and who is in it?

The AI Consortium is a Canadian initiative launched July 7, 2026 by Lightworks, Scotiabank, Sun Life and TELUS to jointly build and govern the enterprise AI control infrastructure required for regulated institutions. Membership is open to qualifying organizations operating at comparable scale and complexity.

What is the Agentic Control Plane?

The Agentic Control Plane (ACP) is the Consortium's flagship program. It is a governance and control layer that sits above enterprise AI agents; it provides visibility, identity, tool brokerage, policy enforcement, telemetry and audit across models, agents, users and inference pipelines. It currently processes more than 2 trillion tokens per month in production across member organizations.

How does this relate to OSFI Guideline E-23?

OSFI E-23 extends enterprise model-risk management to all AI and ML models at federally regulated financial institutions, effective May 1, 2027. A control plane provides the inventory, tiering, lifecycle and evidence infrastructure that E-23 compliance requires; without one, most FRFIs cannot demonstrate policy conformance for every production agent.

Do smaller lenders need their own consortium?

No; smaller lenders cannot economically replicate the engineering investment. The realistic path is to partner with a Canadian vendor whose agents run on your existing LOS, are trained on your policy, and hand back auditable telemetry you own, with no kill switch on your credit decisioning.

How does FundMore protect our credit policy signal?

FundMore agents are trained on each lender's credit policy and refined by that lender's underwriter corrections. The specializing signal stays with the lender; FundMore never pools it across institutions and never originates, funds or brokers on its own account.

What is the fastest first step?

Book a working session; we will map your current agent inventory, policy library and telemetry gaps against a control-plane target state, and give you a 90-day plan that lines up with E-23 and Consumer-Driven Banking timelines.