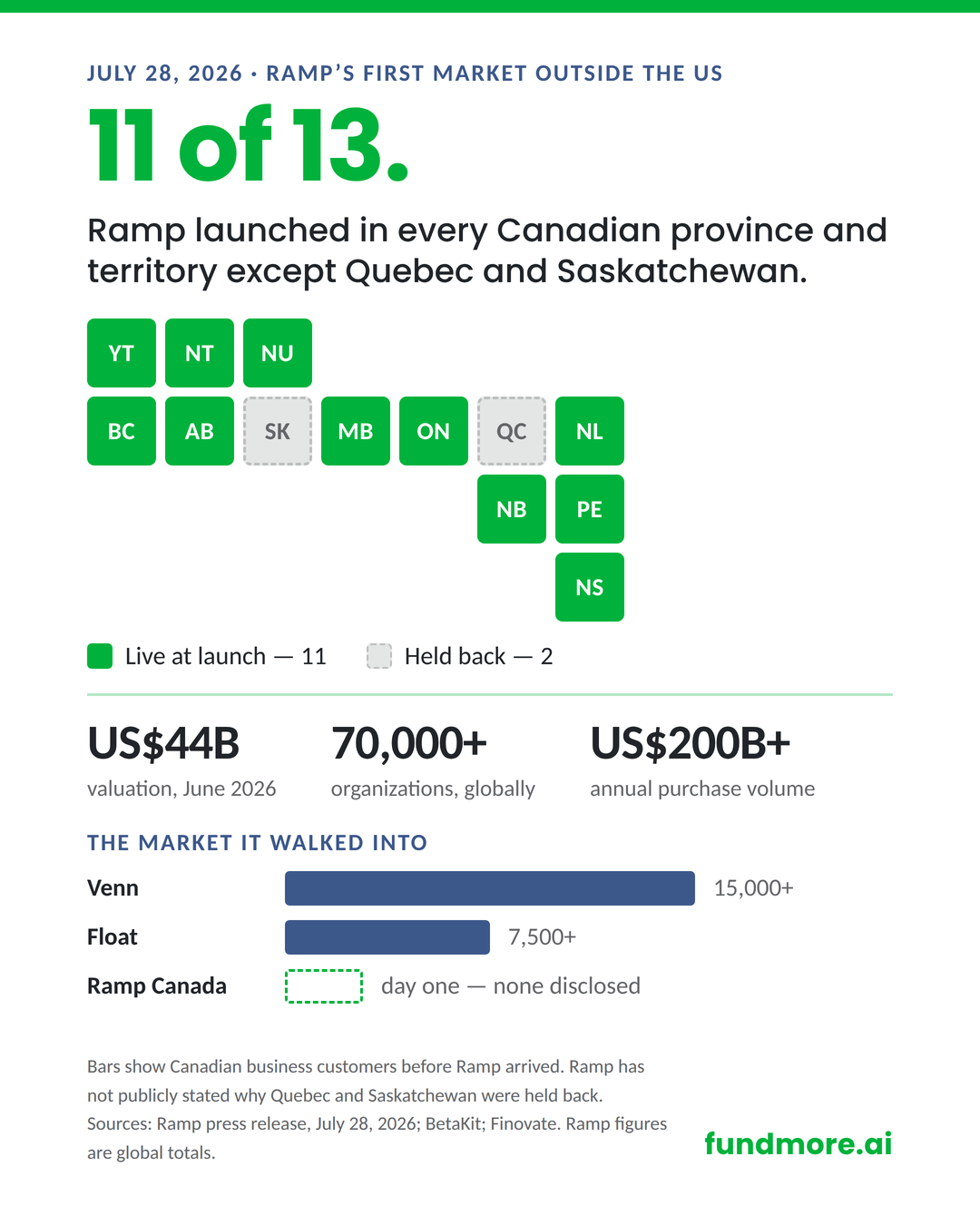

A well-funded US challenger picked Canada. That is a signal worth reading.

On July 28, Ramp officially launched in Canada and opened its first international office in downtown Toronto. It is a genuinely large moment. Ramp was last valued at US$44B after its US$750M raise in June, serves more than 70,000 organizations globally and processes over US$200B in annualized purchase volume. Canada is now the second country on that map.