In seventy-two hours, OSFI made two announcements that, taken together, reshape the competitive structure of Canadian lending for the rest of the decade. On Wednesday, June 17, the regulator confirmed that its Streamlined Framework launches on June 25, creating a faster, more predictable path for provincially regulated credit unions to continue operating as federal credit unions and for fintech “innovators” to become federally regulated deposit-takers. On Friday June 19, OSFI cut the Domestic Stability Buffer to 3.0% from 3.5%, the first move in three years, freeing approximately $74 billion in excess capital across the Big Six and supporting up to $673 billion in additional risk-weighted asset capacity. One regulator. One week. Two levers are pulled in opposite directions, both pointing at the same conclusion.

Recent Posts

On June 9, FirstOntario Credit Union went live on open banking, becoming one of the first credit unions in Canada to activate consent-based financial data sharing under the Consumer-Driven Banking Act. The announcement is significant for one specific reason: this is a Canadian lender that selected its partners 18 months before the rule required it and was production-ready on the day the framework came into force. Most institutions are still drafting strategy decks. FirstOntario's members are already using the capability.

.png)

A national payment system finishes opening its doors

In February, we wrote about the first five fintechs joining Payments Canada; Wise, Float, KOHO, Paramount Commerce, and Brim. At the time, we called it a deliberate policy choice to inject competition into an exclusive ecosystem. Four months later, the policy is doing exactly that.

-1.png)

The risk that defined three years is over

On May 28, 2026, the Bank of Canada released its 2026 Financial Stability Report. The report is the BoC's annual read on systemic risk, and this year's edition contains a sentence every Canadian lender should print out and put on the wall: "we expect this risk to have fully passed by the second half of 2027."

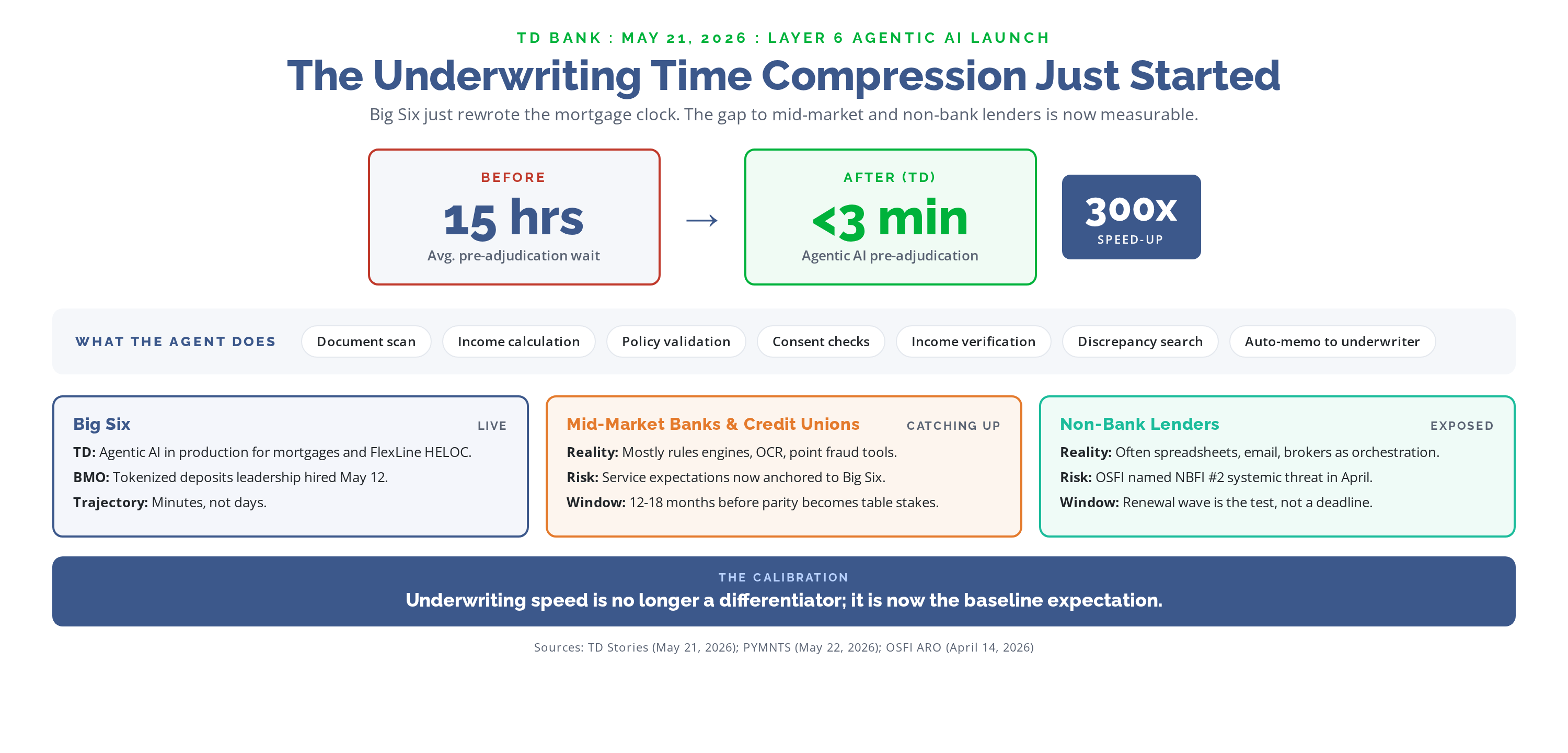

On May 21, 2026, TD publicly detailed its first agentic AI application, built inside Layer 6 and running today across TD mortgage and TD Home Equity FlexLine applications. The model handles document scanning, income calculation, policy validation, consent checks, income verification, discrepancy search, and underwriter memo generation. PYMNTS measured the impact: the pre-adjudication queue, which used to average 15 hours before a human underwriter opened the file, now averages under 3 minutes. That is a 300x compression of one of the most reliably slow steps in Canadian mortgage origination.