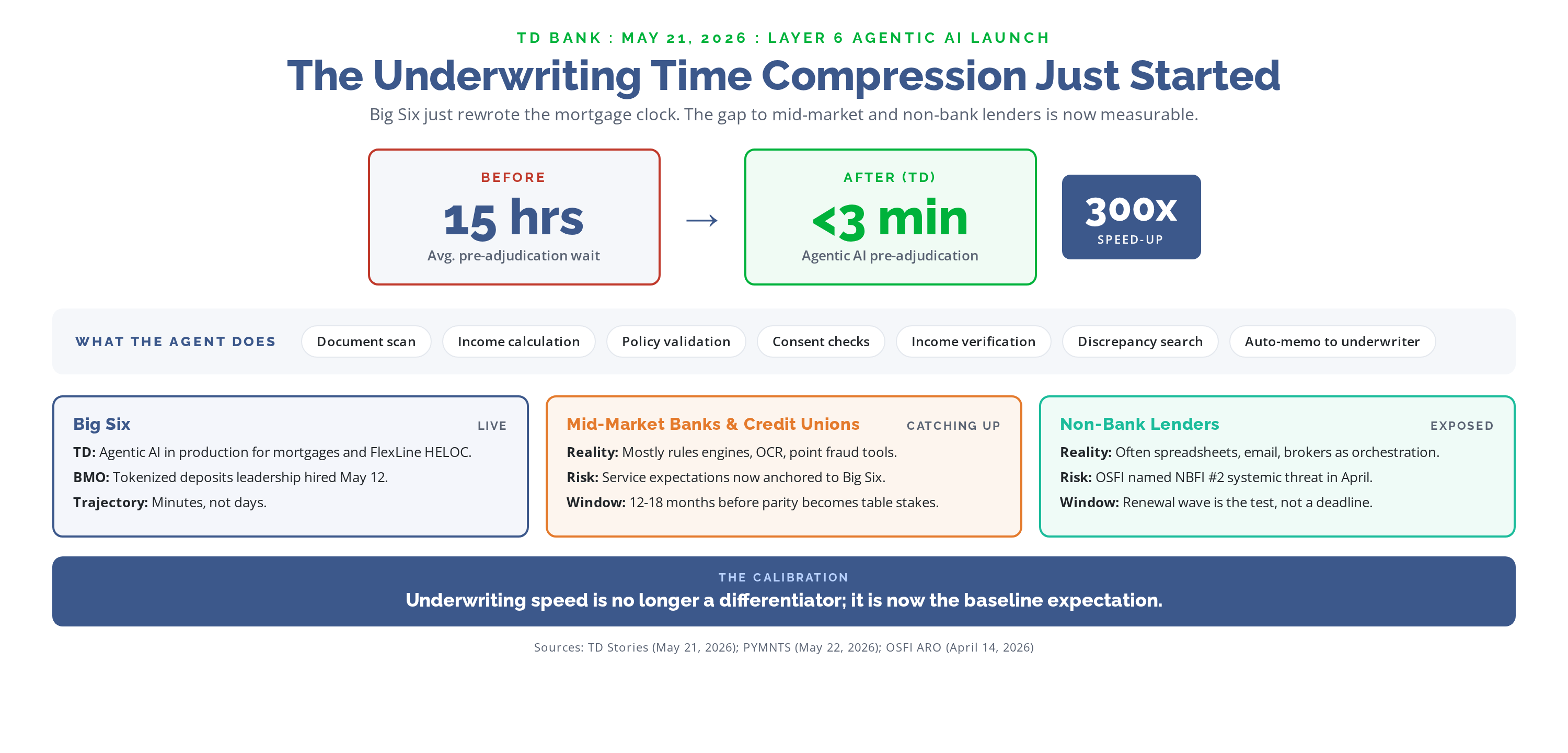

On May 21, 2026, TD publicly detailed its first agentic AI application, built inside Layer 6 and running today across TD mortgage and TD Home Equity FlexLine applications. The model handles document scanning, income calculation, policy validation, consent checks, income verification, discrepancy search, and underwriter memo generation. PYMNTS measured the impact: the pre-adjudication queue, which used to average 15 hours before a human underwriter opened the file, now averages under 3 minutes. That is a 300x compression of one of the most reliably slow steps in Canadian mortgage origination.

Recent Posts

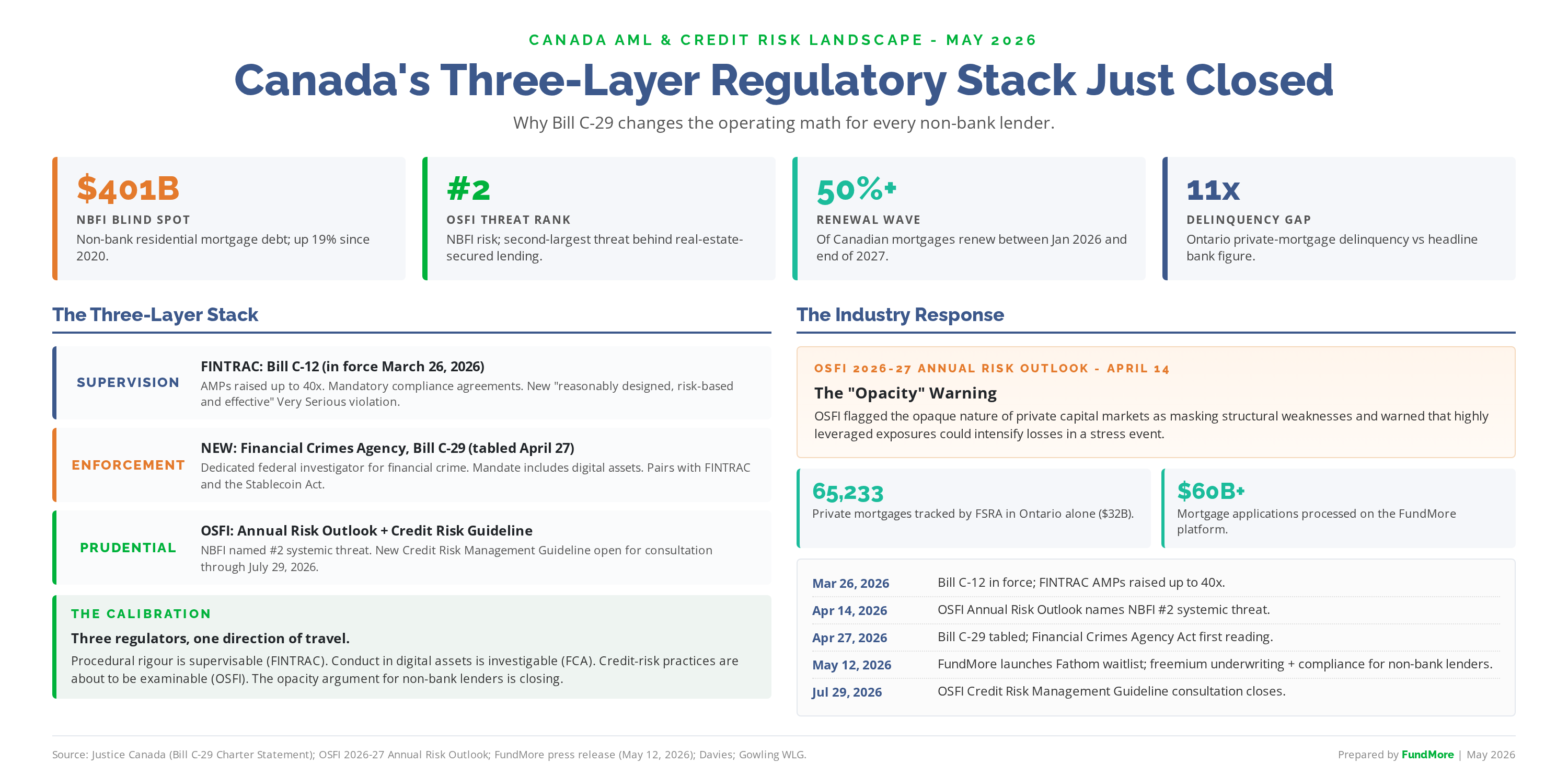

Last week, FINTRAC's public penalty against VersaBank set the calibration for what procedural rigour now costs under Bill C-12. This week, the federal government tabled Bill C-29, the Financial Crimes Agency Act, creating a dedicated federal investigator for financial crime. Read together, the two bills (and OSFI's April 14 Annual Risk Outlook) complete a three-layer regulatory stack that has been signaled for several budgets and is now operational.

On May 5, FINTRAC published its first public penalty against a federally regulated bank in months: a $42,075 administrative monetary penalty against VersaBank, the London, Ontario Schedule I bank. The figure is modest enough that the headline coverage moved past it inside a news cycle. For Canadian AML and risk leaders, that would be the wrong place to leave it.

.png)

Federal economic updates are usually a fiscal exercise. The April 28 release is something different. Layered inside the headline numbers ($37.5B in net new spending, $11.5B improvement to the 2025-26 deficit) sits the most coordinated rewrite of the Canadian financial-services operating environment since the post-financial-crisis Bank Act revisions.

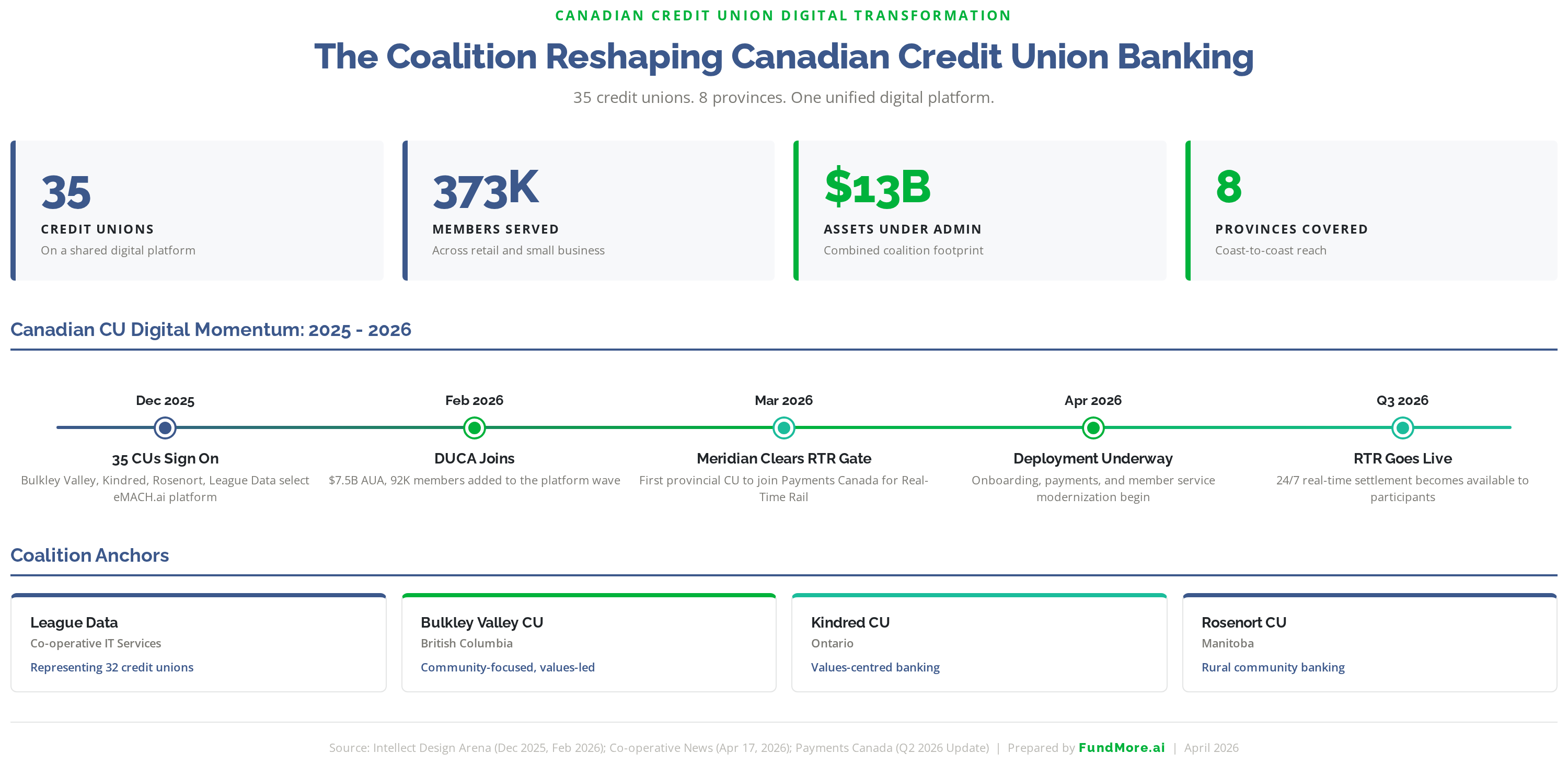

For years the Canadian credit union system was described as fragmented, conservative, and permanently one cycle behind the chartered banks. That description is now out of date.